Focus on the Ending Bank Balance

Most businesses do not fail because they lacked revenue, profit, growth, or valuation. They fail because they ran out of cash.

Because regardless of how attractive a business may look on paper, if the company runs out of cash, the business has a problem. That is the purpose of the CFM.

The CFM helps users evaluate whether a business can survive financially under real operating conditions before capital is deployed.

One of the biggest mistakes people make is confusing acquisition capital with operating capital. They are not the same thing.

A business may appear financeable from an acquisition standpoint, yet still fail because insufficient operating liquidity remains after the transaction closes.

One of the most common mistakes in business planning is assuming that if a transaction can be financed, it should be financed. Those are two different questions. The CFM is designed to help users determine whether an acquisition, startup, or expansion remains financially viable after the transaction closes and operations begin.

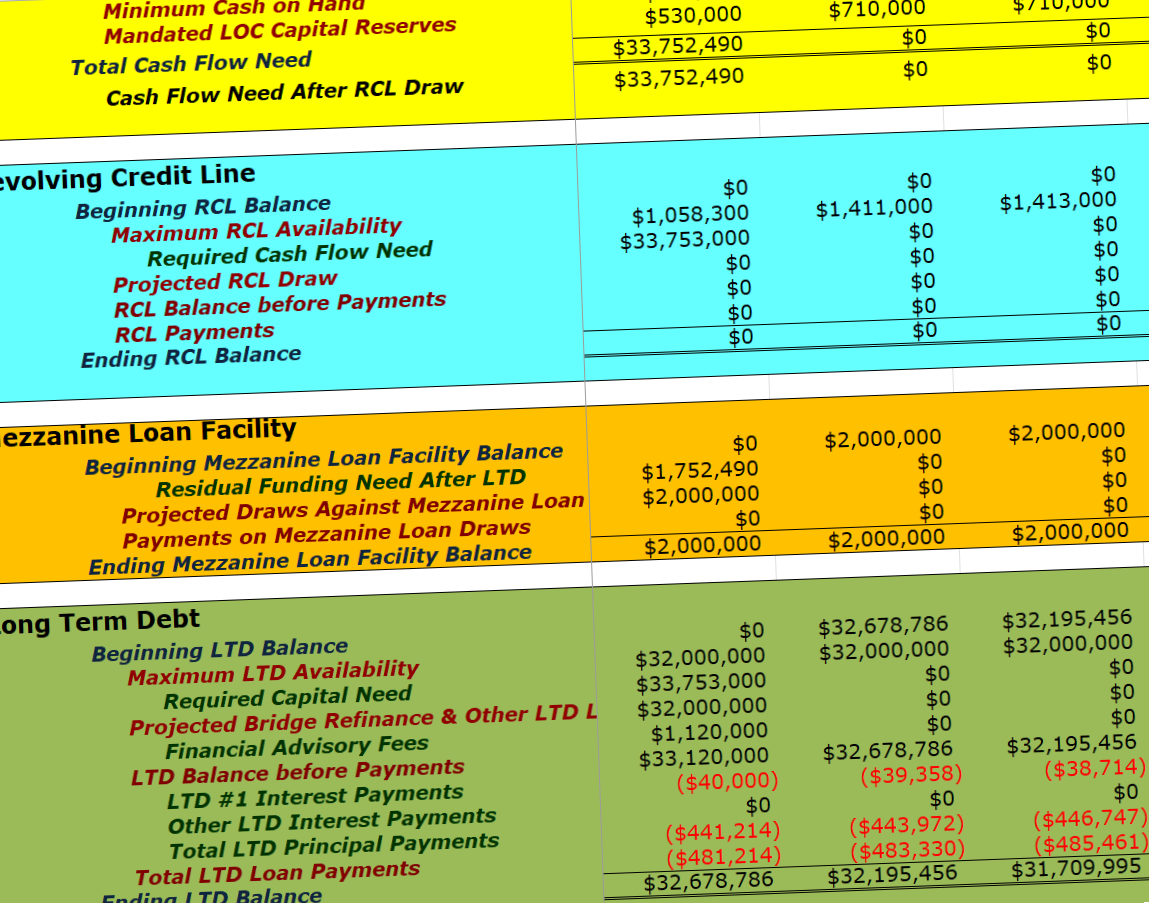

That is why the CFM separates acquisition funding from operational funding. For acquisitions or startups, the CFM typically evaluates capital structure progression through: Cash on Hand → Long-Term Debt → Mezzanine Financing → Additional Paid-In-Capital (if possible) → Preferred Stock → Private Equity

Each layer generally becomes:

more expensive,

more restrictive,

and more dilutive.

If the Ending Bank Balance still goes negative after reasonable assumptions, the conclusion may be straightforward: The acquisition price is too high, the structure is too aggressive, or the business does not presently support proceeding.

That can be difficult to accept emotionally. But recognizing that before capital is deployed is far better than discovering it afterward.

Operational liquidity is evaluated differently. A business may remain fundamentally viable while still experiencing short-term cash pressure during operations. For operational shortfalls, the CFM typically evaluates liquidity progression through: Operating Cash on Hand → Revolving Credit Facility (RCL) → Long-Term Debt → Mezzanine Financing → Preferred Stock

And each layer generally becomes:

more expensive,

more restrictive,

and more dilutive.